If Provision for Doubtful Debts is the name of the account used for recording the current periods expense associated with the losses from normal credit sales it will appear as an operating expense on the companys income statement. As customers delay payments companies may become doubtful of those payments.

Double Entry Accounting Bookkeeping Business Accounting Basics Accounting

The bad debt can result from defaults on notes receivable trade receivables arising through the normal course of business or another type of receivable.

Can i rekod doubtful debt in result. For a doubtful debt create a reserve account also known as a contra account for accounts receivable that may eventually become bad debts estimate the amount of accounts receivable that may become bad debts in any given period and create a credit to enter the amount of your estimate in this reserve account which is known as. Credit Cr Provision for doubtful debts. When you create an allowance for doubtful accounts you must record the amount on your business balance sheet.

Recording decrease in provision for doubtful debts. The accounting records will show the following bookkeeping entries for the bad debt recovery. Having reinstated the accounts receivable balance in step 1 the cash received is now used to clear the balance.

Allowance for doubtful debts is created by forming a credit balance which is netted off against the total receivables appearing in the balance sheet. A doubtful debt is an account receivable that might become a bad debt at some point in the future. If the following accounting period results in net sales of 80000 an additional 2400 is reported in the allowance for doubtful accounts and 2400 is recorded in the second period in bad debt expense.

In practice SARS allowed 25 of the face value of doubtful. An allowance for doubtful debt is an estimate of how much of the trade receivables balance of a business will become irrecoverable in the next accounting period. On top of that companies may also consider any.

Click to see full answer. Record the Cash Received. If a debt is merely doubtful of collection it should not be claimed as a bad debt but should be considered for purposes of a reserve for doubtful debts.

Credit Cr Income statement. For example lets assume that there was a 100 credit already existing in the allowance account. Provisions for doubtful debts are based on the difference between the nominal value of receivables and the amounts considered.

In order to record the adjustment we simply take the 372 and subtract the 100 giving us 272 and we record it as follows. Usually the later the due date is the higher the chances of bad debts are. The fact that a recovery is made after a debt is written off does not negate the correctness of a claim for a bad debt if the recovery could not reasonably have been foreseen at the time the debt was written off.

The allowance for doubtful debt is recorded as a negative balance under the account receivables in the companys balance sheet. This method violates the GAAP matching principle. Debit Dr Provision for doubtful debts.

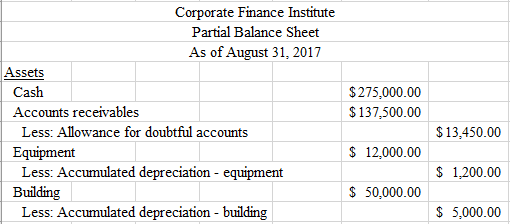

However it may also be temporary. However if there is already a credit balance existing in the allowance of doubtful accounts then we only need to adjust it. Show treatment of Provision for Doubtful Debts in the Balance Sheet of ABC Ltd.

Section 11j of the Act historically provided for a discretion on the part of SARS to allow a deduction for doubtful debts where SARS considered that debt as doubtful. Allowance for doubtful debts consist of two types. The standard conservative accounting rule is that as soon as you have discovered that your debtors are doubtful you must make provisions for such assets.

We record Bad Debt Expense for the amount we determine will not be paid. If you want to record an allowance for doubtful debts and write off as bad debts once confirmed you can make the following entries In each period doubtful accounts are estimated and expensed out by debiting bad debts expense account and crediting allowance for doubtful accounts account using the below journal entry. Recoverability of some receivables may be doubtful although not definitely irrecoverable.

To predict your companys bad debts create an allowance for. Where does provision for doubtful debts go in the income statement. It is exactly what it sounds like an allowance for debts which are considered doubtful.

It may be included in the companys selling general and. Lets say you have a total of 50000 in accounts receivable 50000 X 2. The aggregate balance in the allowance for doubtful accounts after these two periods is 5400.

You you create a doubtful debt it means that these invoices may not be collectible in the foreseeable future. Where the taxpayer cannot claim the debt as bad one may be able to claim a doubtful debt allowance under section 11j of the Act. Bad debts result from the credit extended to customers from a previous transaction.

Specific Allowance General Allowance. Accounting entry to record the allowance for receivable is as follows. The percentage of credit sales method is explained as follows.

If a company and the industry reported a long run average of 2 of credit sales being uncollectible the company would enter 2 of each periods credit sales as a debit to bad debts expense and a credit to allowance for doubtful accounts. It therefore charges 5000 to the bad debt expense which appears in the income statement and a credit to the allowance for doubtful accounts which appears just below the accounts receivable line in the balance sheet. A corresponding debit entry is recorded to account for the expense of the potential loss.

An allowance for doubtful debt can be either a specific debt which is suspected will go unpaid or a more general. However at the time of making this provision the amount and from which debtor amounts will not be recovered cannot be established with certainty. As a result of this the value of the net accounts receivable in the balance sheet does not change.

Allowance for doubtful debt is made to record the losses due to the probability that the debtor may not pay in the future. Debit Allowance for Doubtful Debts Expense Credit Allowance for. For example if 2 of your sales were uncollectible you could set aside 2 of your sales in your ADA account.

We do not record any estimates or use the Allowance for Doubtful Accounts under the direct write-off method. A business makes a provision of 3000 which was 2 of all his trade receivables and a further expected loss of 1200 the total amount owed by one of its customers Franklin who had been. 10 Free Accounting Quiz with answers.

If the doubtful debt turns into a bad debt record it as an expense on your income statement3 Sept 2020 Bad debt expenses are generally classified as a sales and general administrative expense and are found on the income statement. It is deducted from the total account receivables and as a result the most realistic value of account receivables is recorded in. The projected bad debt expense.

Accounting for a Doubtful Debt. 5 provision for doubtful debts is calculated on 500000 5 500000 25000 deducted from sundry debtors. Therefore companies can still recover those debts.

The allowance for doubtful debts is created by forming a credit balance which is deducted from the total receivables balance in the statement of financial position.

Evergrande S Debt Default Sparks Fears In Market Bestcryptotrends Com Debt Investment Advisor Debt Repayment

Bad Debt Overview Example Bad Debt Expense Journal Entries

Bad Debts Depreciation Pre Payments Accruals Emerge 180 Bad Debt Business Risk Debt

Pin On Crafts

If A Company Fails To Adjust Accrued Expenses In 2021 Accounting Books Accounting Cycle Income Statement

India Hunts For Solution To Bad Debt Crisis As Measures Fail Bad Debt Solutions Debt